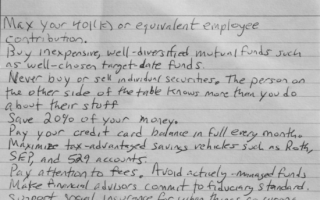

Federal interest rates have dropped for the second time this summer, and now I’m even more tempted to refinance. I crunched the numbers after the earlier price drop, but it would take me a few years to break even. With the current rates and promotions, I could break even in 11 to 12 months.

Closing Costs

If you have never refinanced, you might ask, “Why do I need to break even?” It’s because you have to pay closing costs and fees to refinance – the same as a purchase, though usually much less. Ideally, the reduced monthly payments should offset those upfront costs in the least amount of time possible.

Appraisal

I don’t want to pay any costs to refinance, but I may not be able to avoid it. For starters, I need a new appraisal, which can cost about $500. I currently pay about $50 in private mortgage insurance (PMI) each month because I declined to pay 20 percent of my home’s value as a down payment. Two years later, my loan-to-value ratio is below 80 percent based on estimates from Zillow and Realtor.com. However, to remove the PMI from my fees, I need an appraisal to confirm the property’s value.

When I discussed my options with my current loan servicer, the representative recommended that I refinance to a lower rate to avoid paying for multiple valuations at the same time. While some companies claim they offer no-fee options, they combine the fees into the loan to avoid out of pocket expenses at closing. Somehow, increasing my loan balance seems counterintuitive.

Points and Fees

My other concerns are origination fees and discount points. They are a percentage of the loan paid at closing in addition to processing fees and the appraisal to further reduce the interest rate. My current interest rate is 4.875 percent, and my goal interest rate is 4 percent with no points. I saw several estimates of this scenario with low fees. However, the offered rates did not match.

Pre-Approval

Bankrate and other sites will show you the best rates available. I have an excellent credit score and sufficient assets, so my offers should have been comparable. I received a promotion for refinancing from my bank, and I used their portal for pre-approval. The “rates” tab on the site showed the lowest rate at 4.375 with about $4,000 in closing costs. However, the loan estimate showed the closing costs to be over $7,000, with a credit.

Neither of those scenarios is appealing, so I won’t continue with my application. I could put that money toward my principal directly, save it in my emergency fund, or invest it. If I planned to pay off my mortgage or stay in my house for a decade, then it would make more sense. I would save tens of thousands of dollars in interest. As it stands, that is not in my future, so I will forego refinancing my mortgage and find a better use for my money.

Read More

Is a Cash Out Refinance a Good Idea?

How Soon Should I Refinance My House?

When to Refinance a 15 Year Mortgage to a 30 Year Mortgage

Flanice Lewis is a DC-based financial literacy advocate, blogger, traveler and breast cancer survivor. In addition to having bought her first house at 23, she is a graduate of Howard University and The University of Virginia. You can follow her on Instagram or read her work here on critical financial.

Read More

It's no secret that vehicles are depreciating assets. The second you buy a new car…

I like finding the hidden costs in personal finances. Hidden costs are those costs that…

People sometimes ask how I got into personal finance. The simple answer is by reading.…

We've all wished at some point in our lives that we knew more about finance.…

Due to the pandemic, mortgage rates fell, reaching historic lows. However, since many households…

A lot of home owners don't realize that they are responsible for the water and…

Comments