When thinking about converting from a traditional IRA to a Roth IRA, not only do you have to figure out how much to convert, but you also need to think about when and over how long of a time period.

When using a traditional IRA, you contribute your dollars pre-tax, and you will pay taxes only when you withdraw later in retirement. Roth IRAs are a bit different. You cannot deduct the contributions from your taxes, but when you withdraw later on, nothing is taxed.

In general, the goal is to minimize your taxes. But it’s a bit more complex than that. It also depends on the timing of the tax savings.

The Roth IRA vehicle was only created 20 years ago. It is just now starting to become mainstream. Although most people should probably not convert to a Roth IRA, it is worth it for nearly everybody to at least find out if it makes sense for them. The tax savings could be enormous.

Moving Tax Brackets

If you think you will be in a higher tax bracket when you retire, or if you know you will have very lot tax years coming up, you should definitely look into whether or not a Roth conversion makes sense.

One reason many people cite for wanting to convert a traditional IRA to a Roth is the lure of early retirement. Let’s look at a case study. We have a person, John, who wants to retire when he’s 50. The problem here is that John cannot use his IRA money (without a 10% penalty) until he’s 59.5.

- Transfer all IRA money to a Roth IRA.

- Pay the taxes on the transfer (you will be your marginal income tax rate on this). If possible, pay the taxes out of taxable accounts and not out of the IRA itself.

- Wait at least five years and then begin to withdraw from the Roth IRA, tax-free and penalty-free.

This strategy will allow John to begin using his retirement money at age 55 rather than age 59.5 and he won’t pay the 10% penalty.

Now let’s look at running some actual numbers to see when a conversion makes sense.

Running The Numbers

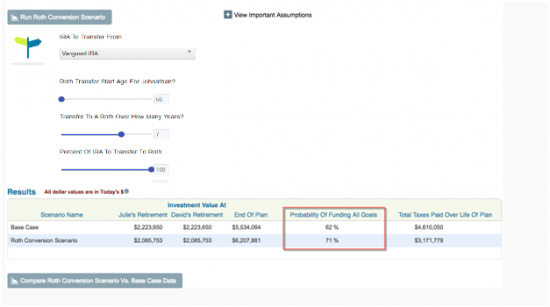

Let’s look at another case study. John and Jane are 54 years old. They plan on retiring next year. They will be start receiving large pensions at age 62 and social security at age 67. Currently their federal tax rate is only 10%, but that will increase dramatically at age 62 when their pensions kick in. This is a perfect example of a couple who should probably do a Roth conversion.

But what if they convert their entire $600,000 IRA to a Roth over a seven year period when their tax rate is low? I ran this scenario and it helps them quite a bit. The results are below:

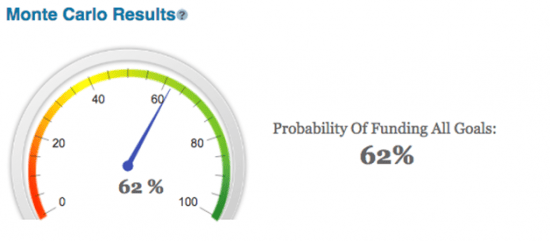

Their probability of never running out of money jumps by 9%. Part of the reason is that their tax burden would decline by nearly 30%, as you see in the table above.

A Roth conversion is not for everybody, but for some it could be a life-saver in retirement.

Photo: CafeCredit.com

Read More

The IRS has finalized new regulations that could catch many retirement savers off guard. Starting…

I like finding the hidden costs in personal finances. Hidden costs are those costs that…

A Roth IRA has long been considered one of the smartest retirement tools out there.…

Roth IRAs are popular for their promise of tax-free growth and withdrawals. But many investors…

Most people know that the earlier they start saving for retirement, the better. But, life…

People sometimes ask how I got into personal finance. The simple answer is by reading.…

Comments