Tweet

Tweet

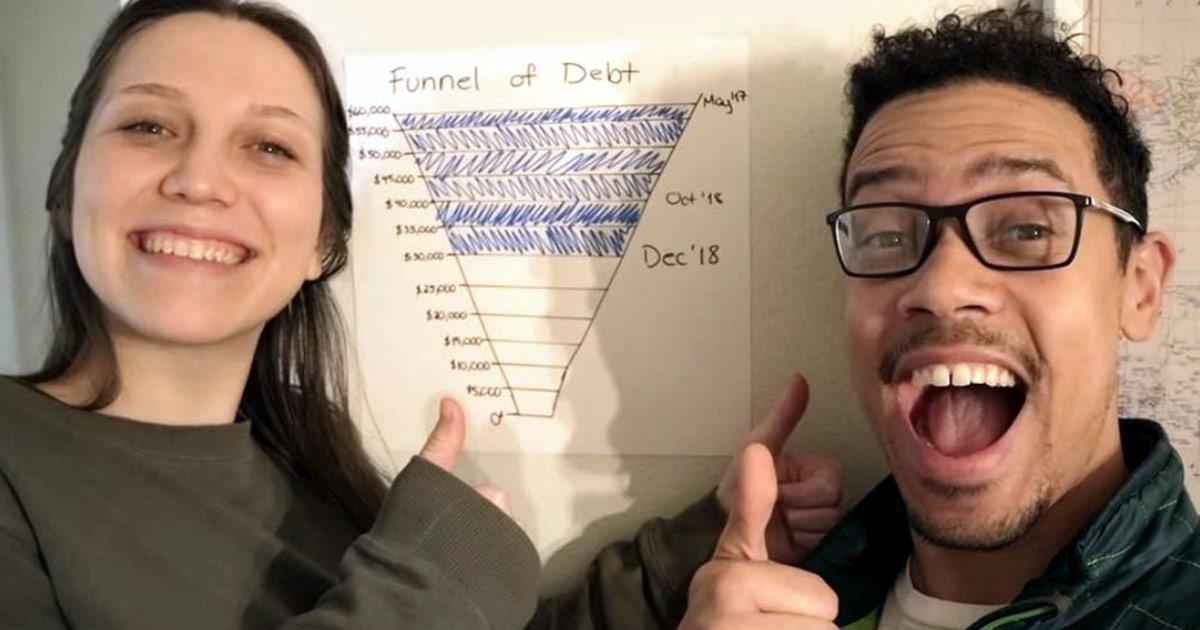

My last post was written before some of the other responses.

I'd recommend you pick up Dave Ramsey's book "The Total Money Makeover" and both read it.

I'm also wondering about the personal trainer certification. Is your husband realistically going to be able to work as a personal trainer given his health status? If he can, that's great and it can bring in added income, but if not, why spend the money to do it?

I'd recommend you pick up Dave Ramsey's book "The Total Money Makeover" and both read it.

I'm also wondering about the personal trainer certification. Is your husband realistically going to be able to work as a personal trainer given his health status? If he can, that's great and it can bring in added income, but if not, why spend the money to do it?

Comment