If this is your first visit, be sure to

check out the FAQ by clicking the

link above. You may have to register

before you can post: click the register link above to proceed. To start viewing messages,

select the forum that you want to visit from the selection below.

Logging in...

Getting close to paying off the house... What then?

Hmmm... I tried to visualize it, and I want to share it with you, but I wouldn't want to clutter your thread. So, you can click here if you want to see it.

Peace,

FrugalDad123

Last edited by FrugalDad123; 08-30-2010, 12:30 PM.

Reason: I changed the link to the appropriate permalink.

Hmmm... I tried to visualize it, and I want to share it with you, but I wouldn't want to clutter your thread. So, you can click here if you want to see it.

Peace,

FrugalDad123

IMO the best way to account for "one time" expenses, is to turn them into annual costs and monthly costs.

For example if a new roof is needed, and you know it costs you $5000 and you need a new roof every 30 years

do $5000/(12*30)=$166 per year or $13/month

And when you retire, add $166 to your withdraw each year, then set that aside in a savings account.

Or move the money from one investment (like stocks) to another investment (like bonds, permanent portfolio or similar). Then when you incur the cost, sell the investment.

If you start adding up the one time items

new HVAC, replacement car, new hot water heater, new roof, you will see the $166 for one item and $3000 for another item and $500 for another item add up. The cool thing is unless Murphy is out to get you, you won't need a new hot water heater, air conditioner and car the same year, so the $3000 you need for annual car replacement and $500 you need for the new HVAC will cancel each other out (all $3500 could be used for the new roof the year you incurred that cost).

The issue is to account for the costs in the budget, and cash flow will solve the problem as long as cash flow either had a fudge factor or similar.

In addition, some costs you control- if you budget $3000/year for 15 years for a $45k replacement car, but the HVAC, roof, and hot water heater all went the year before, I am sure you could either

1) wait 1 year to get the car

2) buy a car cheaper than what you budgeted.

Ray, I think you really have a good portfolio in your hand. I am turning 31 and my partner is turning 30 and we are just building our house in 2011 and I think we still need 3-5 years to finish the loans regarding the house construction until then we will be investing in stocks and other investment vehicle. With all of these, I think we will be needing more years before we can both retire hence; I salute you guys!

Mortgage/Rent (Taxes): $150.00

Water: $50.00

Life Ins: $21.00 Health/Dental: $300.00

Car Ins:$120.00

TOTAL: $3,139.00

What did I miss?

I'm nowhere near retirement, so I'm really just guessing here, BUT ... that monthly expense number for Health/Dental seems a bit low. I'm <25 and I pay $300 in healthcare premiums BEFORE my employer covers additional costs. We also have a $50 per month "sinking fund" for medical expenses in our budget on top of the insurance premiums (to cover deductibles, out-of-pocket expenses, prescriptions, etc.). I'm guessing the only plan I could find for $300/month without an employer subsidy would require an additional out-of-pocket healthcare line-item in the budget of at least $150/month.

The only way I can figure $300/month is if your employer is subsidizing your post-employment healthcare costs through an OPEB plan. Even if that's the case, keep in mind that those OPEB benefits are not guaranteed to the same level as regular pension benefits. At the very least, I would apply a fudge factor to the healthcare costs that reflects a rise higher than inflation over the next 15 years or so.

Also, I'm a little confused on the pension income. It sounds like you'll have 2k/month as of May 2012, but you plan to keep working until somewhere around Oct. 2022. Will you accure additional pension benefits for the extra ten years, or have you already maxed out the benefit accruals? If you've maxed out the accruals, then I'd consider finding another position where your employer will continue to subsidize your retirement income (e.g., find a similar position with a new pension plan or 401(k) with employer match). If you haven't maxed it out, go ahead and consider some of the additional accruals in your retirement income at age 50.

I'm nowhere near retirement, so I'm really just guessing here, BUT ... that monthly expense number for Health/Dental seems a bit low. I'm <25 and I pay $300 in healthcare premiums BEFORE my employer covers additional costs. We also have a $50 per month "sinking fund" for medical expenses in our budget on top of the insurance premiums (to cover deductibles, out-of-pocket expenses, prescriptions, etc.). I'm guessing the only plan I could find for $300/month without an employer subsidy would require an additional out-of-pocket healthcare line-item in the budget of at least $150/month.

The only way I can figure $300/month is if your employer is subsidizing your post-employment healthcare costs through an OPEB plan. Even if that's the case, keep in mind that those OPEB benefits are not guaranteed to the same level as regular pension benefits. At the very least, I would apply a fudge factor to the healthcare costs that reflects a rise higher than inflation over the next 15 years or so.

Also, I'm a little confused on the pension income. It sounds like you'll have 2k/month as of May 2012, but you plan to keep working until somewhere around Oct. 2022. Will you accure additional pension benefits for the extra ten years, or have you already maxed out the benefit accruals? If you've maxed out the accruals, then I'd consider finding another position where your employer will continue to subsidize your retirement income (e.g., find a similar position with a new pension plan or 401(k) with employer match). If you haven't maxed it out, go ahead and consider some of the additional accruals in your retirement income at age 50.

Well, I have to admit, that 300 is a WAG, though I will have VA benefits. I will retire in a Military community so I will have access to Army/VA hospitals (And close to Nashville for emergencies).

I have the ability to retire in 2012 at 20 years of Active Duty Army service... I in no way am planning on 10 more years from that point, maybe 4 more. I will earn 50% at the 20 year mark (in 2012), then earn an additional 2.5% per year after (2013 I will earn 52.5%, 2014 55%, 2015 57.5%, 2016 60% etc).

"The retired pay rate is determined by the average pay rate during the three years when an individual�s pay was highest during his or her military career. That average is multiplied by 2.5 percent for each year in uniform to determine retirement pay. Thus, for 20 years of service, the High-3 formula offers retirement pay equal to 50 percent of average basic pay over the member�s three highest earning years in uniform; 75 percent of average basic pay over the three highest earning years for 30 years of service, and 100 percent of average basic pay over the three highest earning years for 40 years of service."

I agree. Ray you seem to have done really well for yourself.

Thank you all for your kind words, although I could have done a lot better, I am sitting better than anyone in my family and most Soldiers that I have had the honor of working with.

I'm not sure why I have been frugal my whole life but I contribute much of our financial success to my wife, mostly because she's not a spender and agrees fully with our financial plans.

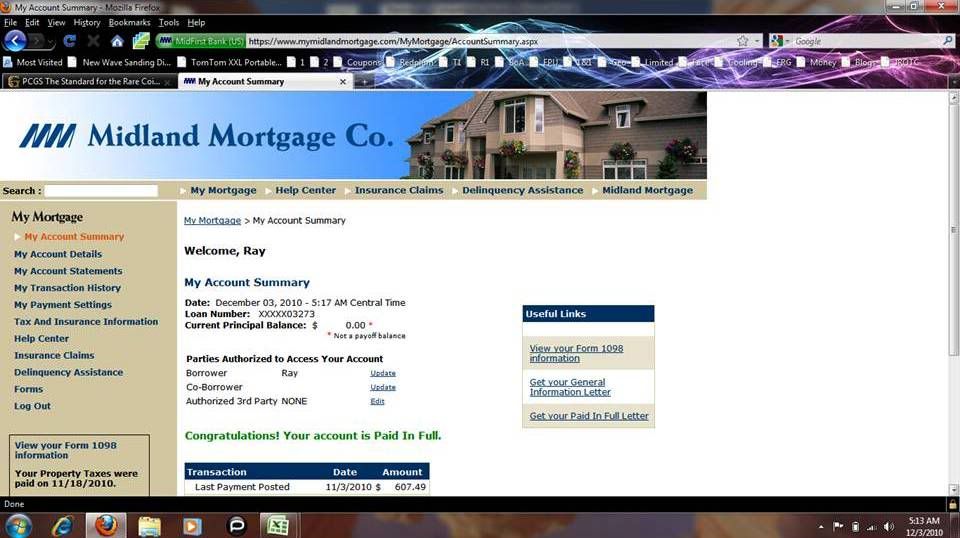

To those of you that have followed my progress and motivated me to meet my goals I say thank you. Yesterday I sent in my final Mortgage payment (A little over 9 thousand dollars) and this morning, this is what I found:

Congratulations!! That is awesome. I love that they actually wrote congratulations on your account. Let us know how it feels next month when there is no mortgage payment.

We recently refinanced our mortgage and plan to aggressively pay it down. I'd love to see a $0.00 balance on our statement in about 7 years.

Steve

* Despite the high cost of living, it remains very popular.

* Why should I pay for my daughter's education when she already knows everything?

* There are no shortcuts to anywhere worth going.

Congratulations! I hope you'll make a start on the next phase in the next month. Both equity and bond markets will continue to be choppy so it will require you shut your eyes, hold your nose and carry on with the plan you chose.

This is a great place to float ideas. You can count on these folks to point out hazards you had not yet considered

Tweet

Tweet

Comment