Originally posted by LivingAlmostLarge

View Post

-

I qualify for one of the exceptions to the 10-year rule since I am less than 10 years younger than him. I get to drain the inherited IRAs over my life expectancy rather than just over 10 years. -

The10 year inherited IRA was a change recent in 2019 secure act. Before there was the stretch option. But now it's also not an RMD but you have to empty it by the end of 10 years, except in the case of your cousin you can treat it like your own but you will start "stretching" RMDs upon death. So you will already have a "level" of income you have to use against the ACA cliff for retiring early.

Leave a comment:

-

You most likely don't want to convert all your pretax retirement money.

1. There are QCDs after age 70.5

2. Tax law may change.

3. Long Term Care Expenses

Leave a comment:

-

You have to make some predictions and assumptions. Will you be in a lower tax bracket when you retire? What will the tax brackets be when you retire? (The Tax Cuts and Jobs Act of 2017 will sunset after 2025 and the tax rates will go back to the previous levels).Originally posted by disneysteve View Post

Some additional considerations. Your MAGI starting when you turn 63 is used for determining whether you pay IRMAA for Medicare.

Your social security is taxed (up to 85% of the benefit) "If your total income is more than $25,000 for an individual or $32,000 for a married couple filing jointly,"

https://www.aarp.org/retirement/soci...-ss-taxed.html

You can most likely stay below certain thresholds in the early years of retirement, but after RMDs kick in it may be more difficult.

And, unfortunately your filing status could change to individual due to the loss of a partner.

One other consideration is non-spousal beneficiaries. Most non-spousal beneficiaries (unless they meet one of a couple of exceptions) will only have 10 years to take distributions on inherited IRAs and 401Ks.

The idea behind doing conversions is not to go into a higher bracket than you expect in retirement. You pay extra taxes now to level out your taxes later.

Which pre-tax accounts to convert? I am not sure if you are referring to IRA or 401K? That decision might be made for you already as a lot of 401k plans do not have the option to do in plan conversions.

If you are referring to tax efficiency--then, pick the one that you expect the most growth for your Roth. For example, bonds in pretax and equities favoring Roth.

I made myself a spread sheet to estimate my taxes over the next 15 years--comparing RMDs vs converting (and paying extra taxes sooner). (Of course, my assumptions are already wrong because the tax law changed--with RMDs at 72.5 and I believe they are updating the longevity taxes and so the RMD formula will change).

Under miscellaneous considerations. If you are under 59.5, you have 2 "qualification" periods. I expect that you have already met the first one and that is you have to have had the Roth open for 5 tax years. If you do a conversion (under 59.5), each conversion also has a 5 year qualification period (which will apply to the gains after conversion). After you turn 59.5--that goes away. So, for example if you do a conversion at age 58.5 --technically you only to meet 1 year for the second qualification period>

https://www.investopedia.com/ask/ans...periodroth.asp

Leave a comment:

-

I just wanted to note that you you don't want to take the money out (it would count as your one and only 60 day rollover for the year). You want to do a direct conversion--which you can do as many as you like during the year.Originally posted by disneysteve View Post

Here is a link to Vanguard "How to convert to a Roth IRA online"

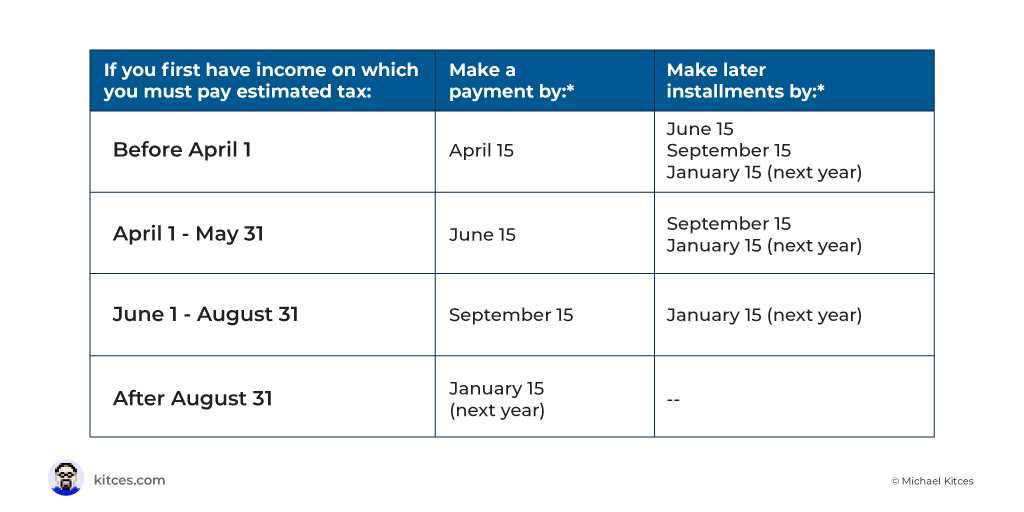

As JustDave mentioned above-- If you do a Roth conversion and you are not 59.5, you will pay penalties on any money that is withheld from the pretax money that is used for taxes. You will want to convert the pretax money 100% and then use after tax money to pay the taxes. You will have several choices to pay the taxes. Since you have a job, you can increase your w2 withholding. IRS does not get upset if your w2 withholding is "lumpy". But, if you do a big conversion in the 4th quarter of the year, and pay all the estimated taxes for just that one quarter--you may have to fill out another tax form to explain because IRS expects the estimated taxes to be 4 equal payments throughout the year and there are under withholding penalties if you don't have a good explanation.

Tax Withholding and Estimated Tax

Instructions for Form 2210

Even if you are over 59.5, as LAL mentioned above your goal should be to use after tax money to pay the taxes.

Leave a comment:

-

Are you converting up to the top of the 10% bracket? If you are in the 0% bracket where do you see yourself in the future? It's a good idea. Are you doing a 401k and Roth ira already?Originally posted by JustDave View PostLeave a comment:

-

You ask the place where you want and you can say I want to pull out $60k and convert. Then you get a 1099R later and you pay taxes on it when you file. You can have taxes withheld but that defeats the purpose. In 2015 and 2016 DH had quit his job. So we had maxed out his 401k for 2015 and 2016, but we also had interestingly 1/2 year of salary both ways. So we decide to pull out and "fill" to the top of the 25% bracket for MFJ which I think was $151k I checked so we calculated our income and did it up to that number. I know we did a $60k conversion in 2016 because we had like $90k in income and decide better to pay 25% then. We also converted I think $60k in 2015 and paid 28%. Mostly because we decided we were filling our 401k and weren't sure when we would retire.

Mostly it's good for Early Retirees who have enough to tide them over until 70 and SS. Because they usually have $50k in cap space of 0%-10% in taxes and then ACA cliff and say you retire at 60. You have 10 years of converting $50k/year so $500k you don't have to grow and RMD till age 72. Based on rule of 7 that would double in the 10 years if you didn't do the roth Conversions and you'd have $1m at age 72 if you didn't do anything. Then you'd be RMD on $1m will be $43890k/year. That plus your deferred SS will kill you on taxes versus converting say that $500k.

Let's say you are 55 and you have 15 years of Early Retirement and $500k in traditional IRA. If you let it double 2x in 15 years you'd have $1.1M. But if you spent 15 years converting $50k/year you would have nothing in traditional IRA, everything in Roth and you've have paid 0-10-12% in taxes along the way. But you need taxable savings to make up the living expenses you'll need since you'll already have $50k in income each year.

Leave a comment:

-

Not sure if I can answer all of your questions, but I did a conversion on my wife's account for the first time last year. It's at Vanguard, so it was just an exchange to another fund. She already had a Roth so I just picked that as the "to" account (I'm not sure how it works if you didn't already have one -- not an issue for you but maybe for others reading). They will send a 1099-R at the end of the year. When you do the exchange you get a popup letting you know it is a conversion and a taxable event.

As to the when, we have 4 kids on a single income. With 8K in child tax credits each year, along with everything else, our federal tax bill is basically nothing, so it seemed like a good time to do it. In retrospect, I should have done it sooner.A conversion is a taxable event and can't be changed.

If you choose to convert to a Roth IRA, your conversion will be final and can't be recharacterized.

Generally, you'll owe taxes on the amount you convert from any eligible retirement account into a Roth IRA for that calendar year. If you've ever made a nondeductible contribution or after-tax rollover to an IRA, you may owe tax on only a portion of this conversion. See IRS form 8606 for more information.

You may maximize the benefit of the conversion if you pay taxes from a separate nonretirement account instead of withholding during the transaction. If you're under age 59� and elect to have Vanguard withhold tax from the distribution you may have to pay a 10% federal penalty tax on the amount withheld. If you choose not to have taxes withheld you'll remain liable for any applicable taxes.

We encourage you to consult a tax advisor about your individual situation.

As to the how much, I had a general idea of how much this would change things tax-wise, so I picked 10K as the amount to start with, figuring I could adjust it in future years. Choosing that same amount every year will take over a decade to convert everything, but we're in our 40s so there is time. Assuming tax laws don't change, blah blah blah.

Hope this helps!

Leave a comment:

-

Educate me on Roth conversions

I always hear folks talking about Roth conversions but it's one thing I really haven't learned about in any detail. I understand the basic concept is that you take a pre-tax account like a traditional IRA or 401K, pull out a portion of the money, pay the taxes due, and then move that money into your Roth. I know that the amount you convert counts as taxable income for that year. But that's about the extent of my knowledge on the topic.

Teach me the details. How do you decide when to start conversions? How do you decide how much to convert each year (at least partly based on tax brackets I believe)? How do you decide, or does it matter, which pre-tax accounts you convert first? And how do you actually go about doing it - like step by step how does it work?

Leave a comment: